If you ever had to choose a health insurance plan, you have probably encountered PPOs. And if you are like most of us, you probably nodded along like you knew what it meant and then secretly Googled it later. You’re not alone in that ignorance, no worries.

PPO stands for Preferred Provider Organization. Sounds fancy, we know, but it just represents the type of health insurance plan that gives you a certain flexibility when choosing hospitals and doctors.

PPOs, unlike other insurance plans, don’t force you to get referrals or stick to a strict network. Like some kind of cool, laid-back cousin of health insurance. But is it right for you? Let’s break it down and see.

How Does a PPO Work?

So, what is a PPO and how does it work?

The PPO plan gives you access to a network of doctors, specialists, and hospitals that agreed to provide medical services at reduced rates, also known as the preferred providers (hence the name). Still, that’s not the best part. The best part is – you don’t have to stick to the network.

When you seek medical care, there are two choices available:

- Use an in-network provider – This is cheaper because your insurance company has pre-negotiated rates with these doctors and hospitals.

- Use an out-of-network provider – You can still see any doctor you want, but it’ll cost you more since they don’t have a special deal with your insurance company.

Also, with PPO, you don’t need referrals to see a specialist. If your skin is acting up, you go straight to a dermatologist. Do you think you need an orthopedic surgeon for your knee? Just make a direct appointment.

This is a huge advantage over HMO (Health Maintenance Organization) plans, which require you to get a referral from your primary care doctor before seeing a specialist. PPOs save you time and hassle by skipping that extra step.

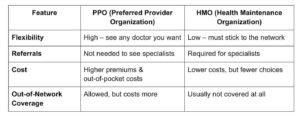

PPO vs. HMO: What’s the Difference?

If PPOs are, as we said earlier, the cool cousin of health insurance, HMOs could be like strict parents. More rules, and while they are good for you, and might save you money, they also significantly limit your choices.

Here’s a quick comparison:

It boils down to this: if you don’t mind paying a little extra for more freedom, a PPO is a solid choice. But, if you would rather save some money, and don’t mind jumping through a few hoops, HMO might be better for you.

What Are the Costs Associated with a PPO?

The truth is, that health insurance is not cheap, and PPOs are on the pricier side. Here are the main costs of the PPO plan:

- Premiums: The amount you pay monthly to have the insurance. PPOs have higher premiums than HMOs, but more flexibility.

- Deductibles: The amount you pay out of pocket before the insurance kicks in. PPOs have higher deductibles than HMOs, so be ready to pay a few thousand dollars before the insurance starts covering costs.

- Copayments: A fixed fee for certain services you have to pay for, even after meeting your deductible, like $30 for a doctor’s visit.

- Coinsurance: A percentage of the total cost after meeting your deductible, like 20% of the hospital bill

- Out-of-Network Costs: If you venture out of network, be prepared to pay a lot more. Insurance still might cover some of the cost, but at a much lower rate than if you stayed in-network.

Pros and Cons of a PPO

Like everything we encounter in life, PPOs have their upsides and downsides.

Pros:

- Freedom to choose any doctor: No need to stick to a network.

- Referrals are not required: You can see a specialist whenever you want.

- Out-of-Network coverage: You’re not stuck with in-network providers.

Cons:

- Higher costs: Premiums, deductibles, and copays are more expensive.

- More paperwork: If you go out-of-network, you might have to deal with claims and reimbursement forms.

- Not for everyone’s budget: If you have to think about money, an HMO might be a better fit for you.

Who Should Get a PPO?

A PPO is a great option for you if:

- You want the freedom to see any doctor you want, even outside your network.

- You need to see a specialist often and don’t want to deal with referrals.

- You travel a lot and need coverage in several locations.

- You don’t mind paying a bit more for convenience and flexibility.

On the other hand, if you rarely go to the doctor and just want the cheapest insurance, a PPO is not worth the extra cost.

How to Choose a PPO Plan?

Not all PPO plans are the same. And, if you’re choosing one, here are some things to look at:

- Check the network: PPOs do allow out-of-network visits, but it’s still best to use an in-network provider when possible, so it is a good idea to make sure your preferred doctors and hospitals are in the plan’s network.

- Compare costs: Look at the premium, deductible, copays, and coinsurance, because a lower monthly premium might come with a higher deductible. Do the math.

- Consider your healthcare needs: High-deductible PPO is not worth it if you visit the doctor once a year. But if you have ongoing medical needs, paying a bit extra for better coverage could save you money in the long run. Again, do your math.

- Look for extra benefits: Some PPOs offer extra perks like telehealth services, wellness programs, or prescription discounts. Pay attention to them, since they could add value to your plan.

Final Thoughts: Is a PPO Worth It?

PPO is a great choice if you love having to freedom to choose your doctors and specialists without feeling like a trained seal. Yes, it will cost you more, but for many people, the convenience and flexibility are worth it.

It’s like choosing between a budget airline and a premium one. Sure, the budget ones are cheaper, if you don’t mind extra fees, layovers, and middle seats. But if you like the smooth ride premium airlines offer, PPO is the way to go.

So, when picking your health insurance, just ask yourself: Do I want the freedom of choice, or do I want to save money? Your answer will tell you if the PPO is the right fit.